2023: The Year That Was

Resilient market and investments upheld amidst challenging economic conditions

The TMT industry has faced its share of challenges over the past year. Inflation and rising energy costs remain a concern, exerting pressure on profit margins and contributing to overall economic uncertainty.

Despite these challenges, telecom services – considered essential by residential consumers – have proven to be resilient; many operators have posted positive results as tactical price adjustments have paid off and customer retention has remained stable. This strategic approach and consumers’ reliance on connectivity has allowed leading providers to sustain modest growth.

The importance of telecoms is supported by the global ambition to deploy fiber and broadband connectivity on a wider scale, with substantial government and private funding ensuring the continued strength of broadband initiatives. For instance, in the UK, the Government’s Project Gigabit has already allocated over £2 billion to broadband suppliers for the rollout of gigabit broadband to rural areas.[1] While in the U.S., $42.5 billion of BEAD funding has been allocated to states and territories by the NTIA, with the states now planning their individual funding programs.[2]

Elsewhere, TMT players have responded to the economic headwinds with cost-saving measures to streamline their operations. Significant workforce reductions have been announced by major operators such as Vodafone, T-Mobile US and most recently, Telefonica.[3]

While 2023 saw a slowdown in industry M&A activity – global telecoms deal value declined by 41% from H1 2022 to H1 2023 – there were notable instances of consolidation and infrastructure divestiture. Notably, Colt completed its $1.8 billion acquisition of Lumen’s EMEA business[4] and Telecom Italia approved the sale of its fixed-line network to US private equity firm, KKR.[5]

In the cell towers market, several Mobile Network Operators (MNOs) divested stakes in joint ventures as part of quick capital-raising efforts.[6] Most recently, Zain, Ooredoo, and TASC Towers agreed to consolidate their tower assets, forming the largest tower company within in the Middle East and North Africa region.[7] Companies like Cellnex have also acknowledged a shift from their aggressive acquisition strategy to concentrating on delivering value from their core business and infrastructure estate.[8]

Looking ahead, until the economy levels out, maintaining profitability will remain the industry’s primary challenge as it balances growth in connectivity and efforts to streamline costs. Refocusing on the core business and customer service will become a dominant theme as cost-cutting measures take effect and price rises increase the risk of customer churn.

![]()

Return on 5G investment has yet to materialize but innovation showcases wireless capabilities

In 2023, deployment of 5G networks in Asia-Pacific markets helped offset the slower deployment in the US, where the initial building is now largely complete.[9]

In Europe, operators are now considered to be lagging, despite being amongst the first to launch 5G networks. The European Commission recently stated that additional investment of approximately €200 billion is deemed necessary to achieve comprehensive 5G coverage in all populated areas.[10] The picture is similar in the UK, where 5G availability across the four MNOs is around 10%,[11] ranking 20th for 5G coverage compared to other European Nations.[12] This has been met by industry calls and government funding initiatives to address rural 5G coverage and prevent further lag.[13]

Achieving 5G ROI remains an ongoing effort within the industry though little improvement has been observed this year. In the consumer market, mobile broadband and fixed wireless access (FWA) remain the primary use cases. Operators are also pursuing enterprise and industrial use-cases, such as private networks and network slicing, to drive new revenue growth.[14] However, enterprise demand for private networks has yet to take off at scale.

There is hope that 5G standalone networks will unlock further innovation, but few commercial platforms have yet been deployed at scale. T-Mobile US – the first operator to commercially launch a 5G standalone network in 2020 – has begun to deploy network slicing this year.[15] Open RAN development is also struggling to gain momentum, as anticipated operator rollouts have not materialized this year. Announcements from operators such as Vodafone and Virgin Media O2 indicate they are still at the early stages of their Open RAN journeys.[16]

While waiting for the materialization of 5G business cases, wireless innovation has not slowed. In the US, Verizon is utilizing mmWave spectrum to offer premium connectivity experiences in all NFL stadiums,[17] addressing the persistent challenge of reliable connectivity in crowded environments. Satellite use cases are also picking up across the US and India in attempts to address rural coverage issues and improved network reliability.[18] Satellite connectivity holds significant promise for network resilience and effective network backup modes.

Despite commercial challenges persisting in 5G, research on 6G is already underway. Notably, South Korea’s SK Telecom is investing in strategic research on 6G capabilities and its use cases.[19] The UK government has also pledged up to £100m in funding to “ensure that the UK is at the forefront of both adopting and developing 6G”.[20] As these first steps are taken, there is a clear need to avoid over-promising on 6G and be more realistic on the MNO business case for deployment.

![]()

The race to roll out fiber in Europe and the UK persists amidst economic challenges

Fiber rollouts continued at pace in Europe, with full-fiber networks in the EU39 countries surpassing 219 million homes, reaching 62.2% coverage.[21] This is up from 198 million homes the year before (an increase of 10.4%).[22]

FTTH Council Europe notes a trend of former incumbents increasing their contribution to fiber coverage, starting to close the gap between themselves and alternative operators.[23] Key 2023 M&A activity in Europe includes the completion of French company Altice’s acquisition of half of Vodafone’s German FTTP operations, a deal worth $1.2 billion.[24]

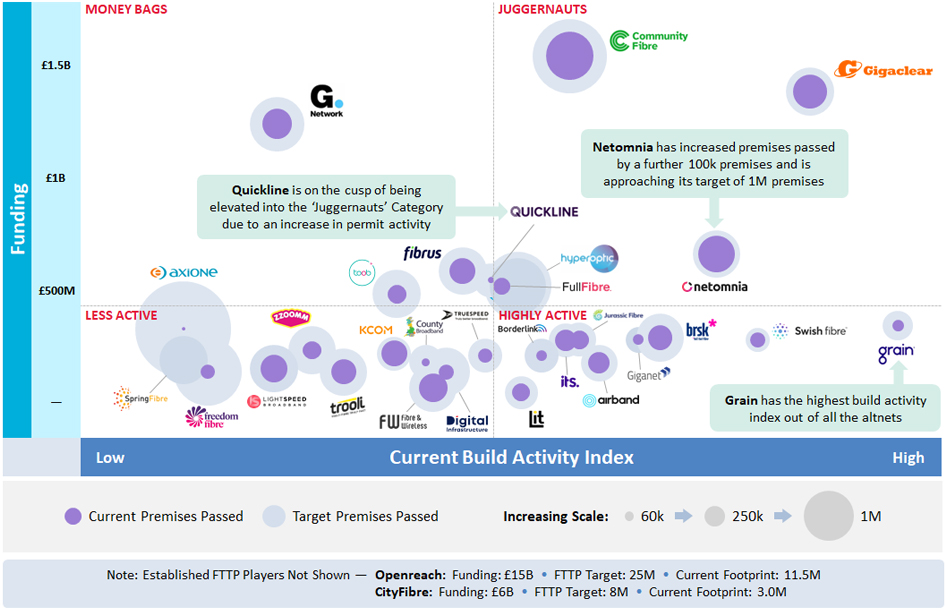

The UK fiber rollout continues to be a tight, well-funded race. Even with increased investor caution and a belief that ‘the goldrush mentality’ is over, funding for Altnets continues. Notable fund raises this year included Gigaclear securing a major new debt facility of as much as £1.5 billion and ITS Technology Group securing £100 million in debt financing.[25] 57% of UK premises have now been reached with full-fiber coverage and 78% are within reach of a gigabit-speed network.[26] While commercial investment is responsible for most of this growth, the impact of the UK government’s £5 billion Project Gigabit is apparent, with over £2 billion having been made available to broadband suppliers.[27]

Recent data shows that Openreach’s FTTP network added a record 860,000 premises to their coverage in a single quarter, now covering 11.85 million premises in the UK.[28] Despite the existence of around 100 UK Altnets, Openreach still accounts for around 80% of the UK’s broadband connections.[29] The largest competing fiber network, CityFibre, reached 3 million premises earlier this year and successfully secured multiple Project Gigabit contracts.[30] 2023 also witnessed the emergence of Nexfibre as a joint venture between InfraVia and Liberty Global/Telefónica. Nexfibre has VMO2 as an anchor customer and its goal is to construct a FTTP network of 7 million premises that do not overlap with VMO2’s existing network.[31] In September, Nexfibre in partnership with VMO2, announced the acquisition of Altnet Upp, accelerating their fiber rollout by 175,000 premises.[32]

While the UK coverage story is good, focus has now switched to customer adoption with many Altnets facing challenges amidst growing competition.[33] Although Openreach has managed to achieve a take-up rate of around one third, many Altnets fall well below this with some remaining in the low single digits, sparking concerns about sustainability.[34] In the face of high inflation and rising costs, cash preservation has become increasingly important. There have been several stories pointing to slowing build rates and job cuts in the sector.[35]

While economic uncertainty has quelled M&A activity for much of the industry, the reverse is true in the UK fiber market as investors seek scale and cost-efficiencies. In September, Fern Trading finalized the consolidation of its four full-fiber networks.[36] In a similar move in October, Basalt Infrastructure Partners LLP, an infrastructure investment firm, announced the merger of Digital Infrastructure and Full Fibre.[37] Other deals include Voneus merging SWS Broadband and Cadence Networks into its operations and acquiring Broadway Partners from administration, and Telcom Group’s acquisition of Luminet which was also finalized this year.[38] As we head into 2024, further consolidation is expected, and we may see smaller firms merge as equals to scale up rather than exit at current valuations.

Updated October 2023, Source: Operator Research, Street Works, News Articles, Cartesian

![]()

US cable broadband growth stalls as fiber and fixed wireless access gain subscribers

Over in the US, cable broadband holds around 65% of US broadband subscribers but saw limited growth this year: the top cable companies recorded only a 0.8% increase in total subscribers in the first half of the year.[39] For large cable firms, mobile is now a key source of revenue growth. Cable Mobile Virtual Network Operators (MVNOs) marked a 41.1% subscription increase year-over-year in Q2 2023.[40] This growth is attributed to investments in fixed and wireless convergence strategies, along with aggressive promotional activities. Comcast and Charter also benefit from favorable wholesale rates from Verizon based on an agreement from 2011.[41] Smaller cable companies may struggle to replicate this success.

Cable’s primacy is being challenged by fiber, with fiber gaining market share as new networks are rolled out.[42] Fiber’s market share is expected to grow from 19.5% in 2023 to 24.7% by 2028.[43] In 2022 we saw the highest annual deployment of fiber ever, and the impact of the United States’ BEAD (Broadband Equity, Access, and Deployment) Program funding will support further increases in coming years.[44] Some cable companies are rolling out their own fiber to expand their service footprints, further boosting fiber’s market share.[45]

The US fiber take-up rate is significantly higher than in the UK’s at 44.7% compared to around 20% in the UK.[46] Despite this, much of the advice at the Fiber Connect 2023 Conference centered on ensuring take-up, not just extending networks.[47] However, challenges to the growth of fiber networks exist, such as labor shortages, labor cost pressures, and inflation, leading to lowered build targets. This has caused some commentators to say that 2023’s fiber construction is likely to be consistent with 2022.[48]

Returning to BEAD, in June, the NTIA announced how the $42.5 billion funding package will be divided between states and territories, with allocations ranging from $27 million for the US Virgin Islands to over $3 billion for Texas.[49] Alaska was awarded the most on a per capita basis due to the high cost of extending fiber to hard-to-reach areas.[50] However, the fact that the BEAD allocation formula only considered unserved, not underserved, locations, and its limited consideration of deployment costs, means that there were winners and losers when it came to the allocation of BEAD funding. This has left some states with insufficient funding to achieve fiber deployment to even those locations below a reasonable ‘extremely high-cost threshold.’[51]

Although the allocation of funds was flawed, project planning continues to move forward. In December, Louisianna became the first state to gain NTIA approval of its BEAD initial plan.[52] The first funding to projects could occur in late 2024, although it will be 2025 before the money really starts to flow.[53] The prospect of new funding entering the fiber market has encouraged private equity companies to invest in fiber too, with companies that are set to receive BEAD funds looking particularly attractive to investors.[54]

Fiber is not cable’s only competition: FWA subscriber growth significantly outweighs net adds to cable companies.[55] S&P Global projects that FWA growth will stabilize over the next year as it continues to garner the majority of industry net adds, resulting in limited cable broadband subscriber growth.[56] The FWA market share is also expected to grow, increasing from 7.3% in 2023 to 15.8% by 2028.[57] Despite this, cable companies claim to not see FWA as a threat due to its inability to meet speed demands, an argument supported by the increasing rate of disconnects seen for FWA.[58] Although, interestingly, large cable firms have started launching wireless offerings.[59]

![]()

Pay TV continues to lose subscribers globally as competition between streaming platforms increases

In 2023, Pay TV providers continued to see revenue and subscriber numbers decrease, as users switch to streaming services and alternative video platforms. While live sports and cable news once kept subscribers loyal to Pay TV, these are increasingly being offered by streaming services, weakening Pay TV’s longtime hold on consumers.[60]

In the US, Q1 Pay TV subscriber losses were higher than in any previous quarter reported.[61] In contrast, streaming services continue to experience user growth. In August, streaming’s share of US TV viewing time was 8% ahead of cable TV – up from a 0.5% difference just one year earlier.[62] In Q3, UK households with at least one streaming service increased by half a million.[63]

The shift in focus away from traditional Pay TV can be seen among MSOs as they pivot towards other solutions. For example, Charter and Comcast’s joint venture, Xumo, offers free ad-supported streaming, both live and on-demand content, integration with streaming apps, and associated hardware.[64] Meanwhile, at Disney, Chief Executive Bob Iger said that some of Disney’s TV networks may no longer be ‘core’ to the company, and Disney is reviewing areas to cut costs.[65]

It should be said that challenges are not absent from the streaming market, as competition continues to intensify and cost-of-living increases bite. In November, Disney announced that it was buying Comcast’s stake in Hulu, giving Disney the ability to test a combined Disney+ Hulu streaming service.[66] Warner Bros Discovery merged its two streaming services, HBO Max, and Discovery+, into one platform, Max.[67] Further mergers are expected going forward. Mobile-based video platforms such as TikTok continue to compete for attention, taking viewing hours away from subscription services.[68]

The screenwriter and actor strikes in 2023 also caused unexpected challenges for streaming services, as numerous US productions were shut down. This impacted streaming services, particularly those with a higher proportion of scripted content, leading to lower content spending and cost of revenues for Netflix than anticipated, which are likely to rise again.[69] However, Netflix’s large share of international content gave the platform some protection from the strikes compared to competitors.

After reporting subscriber and revenue decreases in 2022, a crackdown on password sharing has also increased Netflix’s subscriber base across all regions.[70] The company’s push to monetize homes sharing a password led to Netflix adding 8.8 million net new subscribers in Q3, pushing their subscriber rate to an all-time high.[71] Following in Netflix’s footsteps, Disney’s CEO has announced that Disney+ will also be cracking down on password sharing starting in 2024.[72]

Despite improvements in Netflix subscription numbers, investor confidence is wavering. Netflix shares peaked in July, but then fell nearly 25% in the following three months.[73] While shares jumped back up after positive Q3 results and the end of the actors and writers strikes, the share price is far from its 2021 peak.[74] With its fluctuation in subscriber numbers, revenues, and share price in the past two years, Netflix is one to watch in 2024.

![]()

The impact of AI on telecommunications industry advances

Artificial Intelligence (AI) went mainstream in 2022 following the launch of ChatGPT, OpenAI’s generative AI platform. This launch dominated headlines, sparking discussions on the far-reaching impact of AI, particularly generative AI, on the global TMT industry. Recent forecasts project global generative AI in the telecommunications market to reach $5 billion by 2032, growing at a CAGR of 41.6% from 2023.[75]

For telecommunications providers, the full market impact remains uncertain, but the burgeoning number of use cases primarily centers around three pivotal areas: network management, customer experience, and business optimization. Industry leaders like SK Telecom and Deutsche Telecom have begun taking proactive steps to ensure preparedness for this transformative opportunity, recently forming the Global Telco AI alliance with other major CSPs.[76]

At the heart of industry generative AI discussions is how CSPs can harness AI for network operations and driving efficiencies. Traditional AI and generative AI are being positioned as tools to support network management processes, resource allocation, and fault resolution. This will help operators to optimize network performance, reduce downtime, and decrease network operational costs. Further down the line, AI is tipped to play a pivotal role in 6G network optimization and power efficiency.[77]

Another benefit for the industry will be to further leverage AI capabilities for customer service channels. Whilst IVR menus and chatbots have been used for years, generative AI technology holds the potential to further evolve digital customer service and reduce customer churn. It enables providers to extend support hours, swiftly resolve issues, and free up support teams to concentrate on more complex problems. A recent survey unveiled that 64% of CSP executives anticipate improvements in customer service metrics through AI deployment,[78] with companies like Lumen already piloting new Microsoft AI tools to enhance their customer service.[79] Moreover, generative AI technology can be embedded into broader CRM strategies to drive sales and brand loyalty by analyzing customer behavioral data to deploy hyper-personalized customer offers.[80]

AI also presents opportunities for workforce optimization, by streamlining operations and enabling businesses to run more efficiently while reducing headcount. Large network operators are increasingly seeking efficiency and agility through AI-driven automation, with companies like BT planning significant workforce reductions, with at least 10,000 role reductions attributed to automation and digitization.[81]

However, the full impact of generative AI remains unknown, and the regulatory landscape is likely to evolve. A recent survey revealed that 76% of digital service provider (DSPs) leaders acknowledged the power of generative AI, but that it required regulation.[82] DSPs are encouraged to begin preparation for an AI-dominated future, ensuring their services are prepared to meet increasing internal and external demand. Colt’s CEO recently hailed their acquisition of Lumen in putting them in a strong position to meet the growth in enterprise AI usage.[83] Networks must promptly assess if they have sufficient network and data infrastructure, skilled workforce, and strategic partnerships in place to meet the changing market dynamics.

![]()

Do you agree with our predictions? What do you think 2024 will bring to the communications sector? Share your comments on our Year-End Letter with us.