Addressing the USA Broadband Availability Gap: Expected Funding and Scenario Planning for States

By Michael Dargue and Sarah Pettengill

Introduction

The Broadband Equity, Access, and Deployment (BEAD) program holds out tremendous opportunity to close the broadband availability and adoption gaps through its $42.45 billion in funding. Although final funding amounts will not be known until 2023 when funds are allocated, States can gain insight today on available funds and expected CAPEX requirements to prepare their Action Plans and funding proposals.

Working in partnership with ACA Connects, we developed a framework and approach for States to:

- Estimate their eligible unserved and underserved locations based on the latest FCC data, with adjustments for the known under-reporting of unserved locations, commitments from other funding programs, and expected incremental builds through 2024

- Anticipate their share of the $42 billion in funding based on the BEAD guidelines on minimum allocations, high-cost allocations, and remaining funds allocations

- Estimate the additional contribution from match funding

Using our propriety network cost model, we estimated the average cost per location for each census tract by state using premises location data, network routing algorithms, and benchmark industry costs to evaluate the expected funding received by each state and resulting fiber deployment feasibility.

Our Approach and Results

To aid states in developing their action plans, we devised two scenarios that provide a perspective on the range of fiber that States will be able to deploy:

- Scenario 1: Baseline Fiber illustrates the funding required to deploy fiber – the priority technology in the NTIA NOFO – to all unserved and underserved locations below a reasonable “extremely high-cost threshold.” Other technologies are used to serve the remaining locations, with any remaining funds held back for affordability and other eligible programs

- Scenario 2: Maximum Fiber reflects the maximum fiber reach achievable, considering all eligible locations with funding above the high-cost threshold

States and Territories must consider which strategy to pursue as they design their Action Plans.

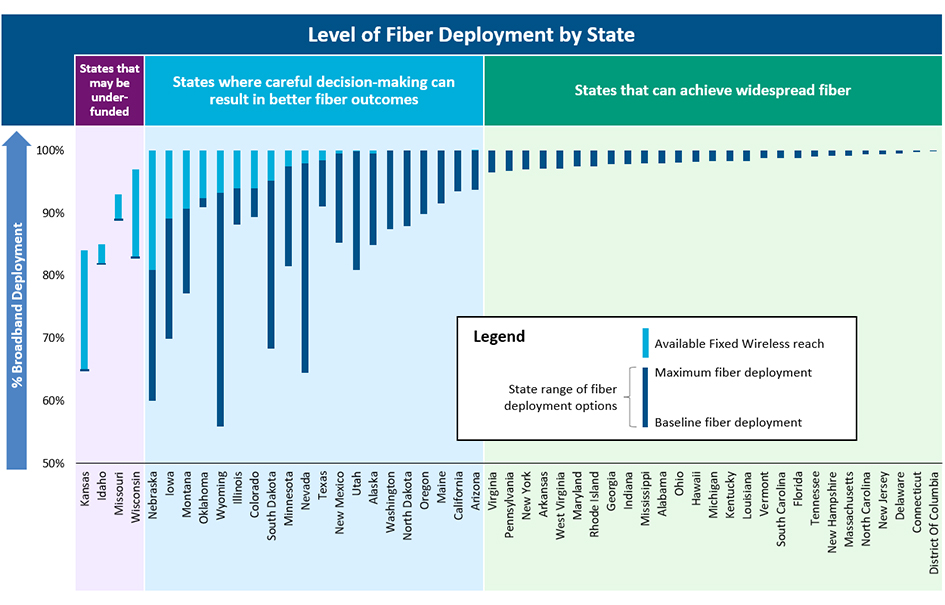

The chart below highlights the range of fiber deployment for states under the two scenarios. Our results indicate that some states are in a more favorable position that others based on the BEAD funding legislation. BEAD will award a fixed amount per unserved location to each state. Aside from the fixed premium per high-cost unserved location, there is no consideration of cost differences between unserved locations which leads to winners and losers:

- 53% of States (incl. Washington DC) can reach 100% of eligible locations with a full fiber deployment under the maximum fiber scenario and retain additional funding for affordability and other eligible programs

- 39% of States can achieve the baseline fiber deployment scenario with sufficient funding to reach remaining eligible locations with alternative technologies through fixed wireless or other technologies.

- Four States (Missouri, Idaho, Wisconsin, and Kansas) are expected to have insufficient funding to achieve the baseline fiber deployment scenario and cannot reach 100% coverage, even with alternative technologies.

Key Considerations for States

State broadband offices can act now to plan accordingly based on their estimated funding allotments. As planning commences a key decision will be setting the extremely high cost per location threshold at a point which maximizes the benefits for local communities. For states that anticipate funding constraints, now is an optimal time to consider the following questions:

- How far are states willing and able to reach with fiber, given their broadband program objectives?

- Are alternative funding sources an opportunity for the state, whether state-specific matching or other sources of funding? These funding sources could include:

- Private companies

- Nonprofits, cooperatives, utility companies

- Regional planning or governmental organizations

- Federal regional commissions or authorities

Conclusion

Closing the broadband availability gap is a once-in-a-generation opportunity to provide connectivity and broadband access to previously marginalized locations. Before funding announcements are finalized, States and Territories should act to determine their unserved and underserved locations, finalize fiber deployment objectives, evaluate their likely anticipated BEAD funding allotment, and initiate planning to achieve their broadband program goals.

To learn more about our study with ACA Connects, contact Cartesian