Watching Sports Is Hard. Partnerships & Technology Can Fix It.

Trouble finding the game recently?

The rise of cord-cutting and over-the-top (OTT) streaming has led to significant fragmentation of sports content, media, and broadcast rights. Major sports leagues are negotiating these agreements with many OTT streaming platforms like Amazon Prime Video, YouTube TV, and Netflix—not just a handful of cable networks.

The increasingly fragmented sports media landscape is causing pain for consumers and churn risk for providers. Younger sports fans prefer to use streaming platforms over cable to watch sports, marking a particular challenge for traditional players.

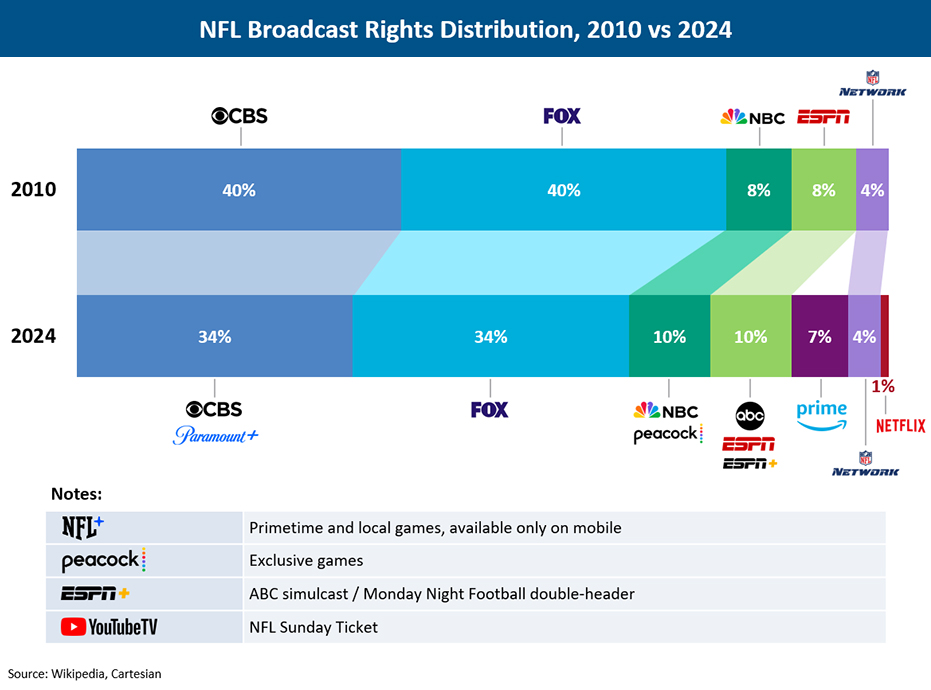

Consider this trend in the context of the NFL, the largest sports audience in the US by far. As recently as 2010, American football games were aired exclusively by networks like CBS, FOX, NBC, and ESPN. Now, that content has become split across thirteen different broadcasters and OTT streaming platforms, four of which are streaming native.

Methodology: Distribution of broadcast rights for each network/streaming service were parsed from various sports media sources, then estimated total games per season based on the number of games per week for each season each network/service broadcasted.

Winners & Losers in Today’s Sports Streaming Landscape

Sports leagues are the clearest beneficiaries here: The more sports media rights fragment, the stronger their negotiating position becomes and the higher the price they can command. The NBA recently closed a massive deal with ESPN/ABC, NBCU and Amazon Prime Video worth $76 billion over 11 years. That’s a 160% per season increase over the league’s previous arrangement.

For consumers, it means a harder time watching games, and higher costs for accessing them. It would cost almost $800 to get access to every NFL game this season. That’s on top of needing to pay for internet service and a TV. Even Sunday Ticket, the most cost-efficient way to get the most NFL games at $479 for the season, excludes digital-only events.

For providers, it’s become increasingly difficult to deliver a seamless sports-viewing experience to customers, despite the demand for it. The result: Serial churn, long-term retention problems, and lost revenue.

In 2024, the Walt Disney Company, FOX, and Warner Bros. Discovery attempted fix this with Venu, a sports-specific OTT service. It would hold nearly 60% of all U.S. sports broadcast rights. The platform’s launch was halted amid a challenge on antitrust grounds.

The halt of Venu does not mean that consumers need to be stuck in this fragmented sports ecosystem forever, though. In fact, these challenges present a unique opportunity for providers.

“Re-Bundling” Through Partnerships

Partnership strategies can benefit everyone. By turning service providers into integration points for sports content, sports fans can find and watch the sports through a single interface.

Hard-bundling bakes new services into the core offering, and soft-bundling enables consumers to select services they want a la carte. The ease of signing up and getting started on most OTT platforms provides opportunities to experiment with dynamic or sliding scale bundle pricing models – potentially by the sport or event.

Mobile devices and 5G connectivity make it possible to watch sports practically anywhere. Telecom providers can develop mobile-first sports viewing experiences through partnerships with mobile operators, or increasingly through their own converged experience. Picture-in-picture technology, multi-angle views, real-time stats, in-game social interaction – these next generation features deepen the game-watching experience.

The best customer experience for the best value will win, and competition to secure the front-porch to the sports streaming world is fierce.

Stitching a new experience together is not trivial. Service providers should develop flexible product roadmaps that balance internal capabilities, partner relationships, and the challenging technical realities of seamless integration. Questions emerge quickly, and smart providers are building strategies to structure their thinking through tradeoffs:

- Who should we focus on competitively? SVODs? Smart TVs? MVPDs? MNOs?

- What matters the most to customers now? In 5 years?

- How do we capture value while reducing friction to subscribers?

- What are the integration requirements from partners?

- What new capabilities are needed internally? When?

How Cartesian can help

With decades of experience in video product quality, content strategy, and sales & marketing analytics, Cartesian can help telecommunications and media companies develop strategic roadmaps and television platforms that drive innovative, industry-leading entertainment experiences for their customers.

Contact us today to learn more.